Many mobile game developers are still adapting to Apple’s privacy changes which, combined with post-pandemic declines and major shifts in the gaming industry, is proving a lot to contend with when attempting to scale a game.

Despite these market changes, some regions are still managing to thrive, such as the Middle East and North Africa. In this guest post, Sandsoft Games, VP of Marketing Ratko Bozovic shares valuable insight into the expanding MENA region and why its approach to user acquisition could present promising opportunities for developers who embrace the market at an early stage.

Apple’s changes to the identifier for advertisers triggered a seismic earthquake in the mobile games market. The foundations on which the entire sector was built upon were shaken by app tracking transparency, and publishers can no longer easily find players that will engage with their games, let alone spend in them. Now, Apple’s Privacy Manifests aims to put an end to fingerprinting, too, causing another rupture in the ecosystem.

Amid the changes, the latest data.ai and IDC reports estimate global player spending in mobile games dropped by 5% year-over-year in 2022, the first yearly decline on record, with a further 2% decline forecasted for 2023. Despite that drop, the sector is still predicted to generate an estimated $108 billion (56% of the overall gaming revenue) and it remains the most significant market potential for the gaming industry.

The Middle East and North Africa (MENA) was one of the few to grow through the post-pandemic, post-ATT slump.

Ratko Bozovic

It should be noted that while ATT has clearly had a substantial effect on the decline, other factors such as global macroeconomic conditions, inflation, the energy crisis and comparisons to oversized gains during the pandemic and lockdowns were also factors in driving revenue downward.

The rule changes have impacted all markets, but some regions have fared better than others. In particular, the Middle East and North Africa (MENA) was one of the few to grow through the post-pandemic, post-ATT slump. And, as global markets return to predicted modest growth, MENA is poised to deliver a far larger upside.

MENA’s resilience and growth as an emerging market

Newzoo reports that the Asia-Pacific region suffered the largest decline in 2022, with revenue falling by 8.9% Y/Y to $84.8 billion. Despite this, it still represents 46% of global games market consumer spending. North America and Europe, meanwhile, saw declines of 2.5% and 2.4%, respectively.

The fastest-growing region? MENA. Revenue in 2022 was up 5.8% Y/Y to $6.8 billion. Latin America was the only other region to experience growth, as consumer spending rose by 3.3% Y/Y to $8.4 billion. Newzoo credits growth in these regions to new players entering the mobile games ecosystem and better access to payment methods.

Delving deeper into the region’s growth, Niko Partners’ MENA-3 Games Market Report claims that Saudi Arabia, the United Arab Emirates and Egypt alone generated $1.79 billion in 2022, a slight increase from 2021’s $1.76 billion. Interestingly, while 58.2% of gamers in these countries are based in Egypt, Saudi Arabia accounted for 58.7% of revenue. Niko Partners forecast these countries will generate an extra $1 billion combined by 2026, accumulating $2.79 billion.

Of course, it should be noted that global markets are predicted to return to growth over the next few years, with Newzoo anticipating the industry will be worth as much as $206.4 billion by 2025, growing at a CAGR of 2.9% since 2020.

How this growth will actually pan out remains to be seen, though hopefully, the macroeconomic factors touched upon previously will have eased by then. But in MENA, more of the young population will gain access to mobile devices, payment systems and games – both homegrown and global – creating a larger market at warp speed.

User acquisition and cultural differences

Even in a growing market, overcoming ATT and various upcoming privacy policies from both Apple and Google is a significant challenge.

When it comes to user acquisition in MENA, CPIs in the region are modest compared to major markets in the U.S. and Western Europe. Still, some countries, such as Saudi Arabia, offer access to a high-spending audience. A SocialPeta whitepaper analysing the mobile games marketing space in H1 2022 detailed the top 10 countries for average CPI costs. South Korea ranked the highest at $13.9, while the U.S. averaged $7.68 and Germany $5.14. No MENA countries ranked in the top 10.

The usual suspects, such as Facebook and Google, are still the go-to channels for marketing. Snapchat is also hugely popular in the region, ironically thanks to its privacy-focused messaging, and can potentially be a valuable tool in finding new players if they only manage to tweak their algorithms to be more focussed on direct response instead of brand campaigns. In 2020, Snapchat was said to have a reach of 50% of 13 to 24 year-olds in UAE and 90% of 13 to 34 year-olds in Saudi Arabia. Meanwhile, 85% of daily users interacted with its lenses every day.

While UA targeting remains an issue given the privacy landscape, the MENA market is actually quite open to sharing data with their favourite games.

Ratko Bozovic

The region, and the Middle East in particular, is known for its preference for privacy – one of the reasons an app like Snapchat is so popular. This extends to the physical world too for example, with many residents in the region choosing to build high walls around their homes to stop others from seeing inside.

It’s perhaps unexpected, then, that while UA targeting remains an issue given the privacy landscape, the MENA market is actually quite open to sharing data with their favourite games.

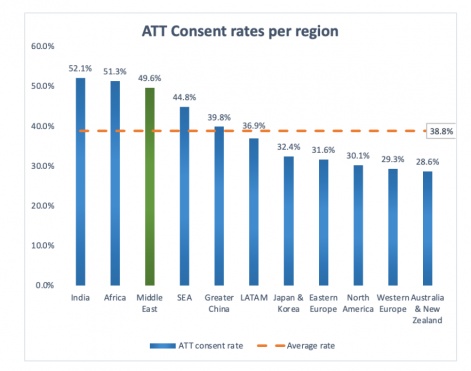

According to data from mobile marketing analytics platform Appsflyer, ATT opt-in rates for the App Store’s games category reached an average of 38.8% in Q2 2023. Analysing rates by region, the Middle East had the third-best opt-in rate in the world at 49.6%, just behind the Indian Subcontinent (52.1%) and Africa (51.3%). For comparison, Western Europe had a rate of 29.3%, while North America had 30.1%.

By country, Cambodia ranked No. 1 with a 74% opt-in rate, while Middle Eastern countries like Iran and Iraq ranked No. 2 and No. 3 with 70.5% and 62.4%, respectively. Key MENA countries like the United Arab Emirates still ranked highly with 52.5%, Saudi Arabia had a rate of 51%, and Egypt 41.8%. One of the world’s top mobile games markets, The United States had an opt-in rate of 29.9%, while China had 36.3%.

MENA opportunity

ATT is a challenge that faces all developers and publishers looking to scale their games or even maintain the status quo. However, emerging markets offer an opportunity to grow at a reasonable cost, with regions like MENA continually seeing more consumers get access to content and services that enable them to spend on games. Additionally, MENA countries are home to a large, young and tech-savvy population that is hungry for new games and gaming experiences. This presents a massive opportunity for game developers to capture this growing market and create successful and profitable games.

There are countries in MENA, such as Saudi Arabia, that already have high-spending players. As the region grows, it’s an opportunity to enter the market early. It also offers a counter to the mature global markets, with plenty of room to grow despite heavy industry headwinds that sparked a global gaming decline.

Edited by Paige Cook

Discover more about the latest trends and updates for indies and AI at Pocket Gamer Connects. In this video, from Pocket Gamer Connects Helsinki, Mahmoud El-Azzeh, VP of Product at Carry1st, discusses Africa: The Next Frontier in Mobile Gaming.