The report cites two reasons for the slowdown in foldable phone shipments. The first reason, says TrendForce, is that consumer retention is low as first-time owners of these devices have been experiencing maintenance issues with these phones. This, says the report, has led to a “lack of confidence” in foldables. The result, says the report, is that consumers aren’t buying a second foldable and are turning to flagship phones instead.

Huawei’s new Pocket 2 clamshell sports four cameras

The second reason has to do with the pricing of these phones. Pricing has yet to, “reach the sweet spot for consumers,” TrendForce says. The report notes that mass production of key components such as Ultra Thin Glass and hinges could help bring down their prices eventually resulting in lower costs to consumers. Additionally, Chinese panel suppliers are increasing their shipments and these firms charge less for their foldable panels than the Korean display companies such as Samsung Display and LG Display.

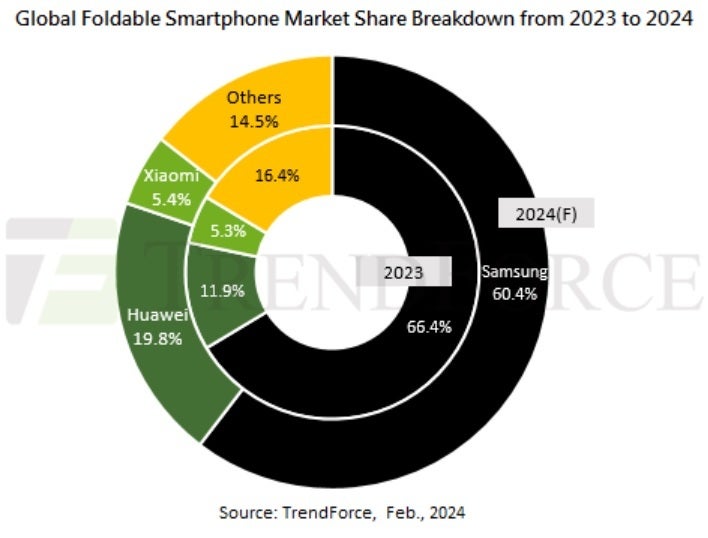

2023 foldable market shares and 2024 forecasts

For this year, Trend Force expects Samsung to stay on top with 60.4% of the foldable market, and Huawei, which just announced its quad-camera Pocket 2 clamshell, is aiming to take 19.8% of the market with aggressive shipments of its foldable devices. Huawei is also rumored to be working on a tri-fold foldable as is Samsung and this could give the foldable market a much-needed shot in the arm.